Futures Market: Overnight, LME copper opened at $9,398.5/mt, initially bottoming at $9,379.5/mt amid fluctuations. The center then rose, peaking at $9,425.5/mt during the session, followed by slight fluctuations and a decline towards the close, ultimately settling at $9,382.5/mt, down 0.87%. Trading volume reached 15,000 lots, and open interest stood at 300,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 76,740 yuan/mt, initially bottoming at 76,680 yuan/mt. The center then rose, peaking at 77,030 yuan/mt during the session, before declining and consolidating sideways towards the close, ultimately settling at 76,860 yuan/mt, down 0.81%. Trading volume reached 22,000 lots, and open interest stood at 169,000 lots.

【SMM Copper Morning Brief】News: (1) US Fed - Harker: Current economic conditions support maintaining a stable interest rate policy for now; Bowman: Stronger confidence in inflation decline is needed before further rate cuts. Inflation is expected to decline, but upside risks remain.

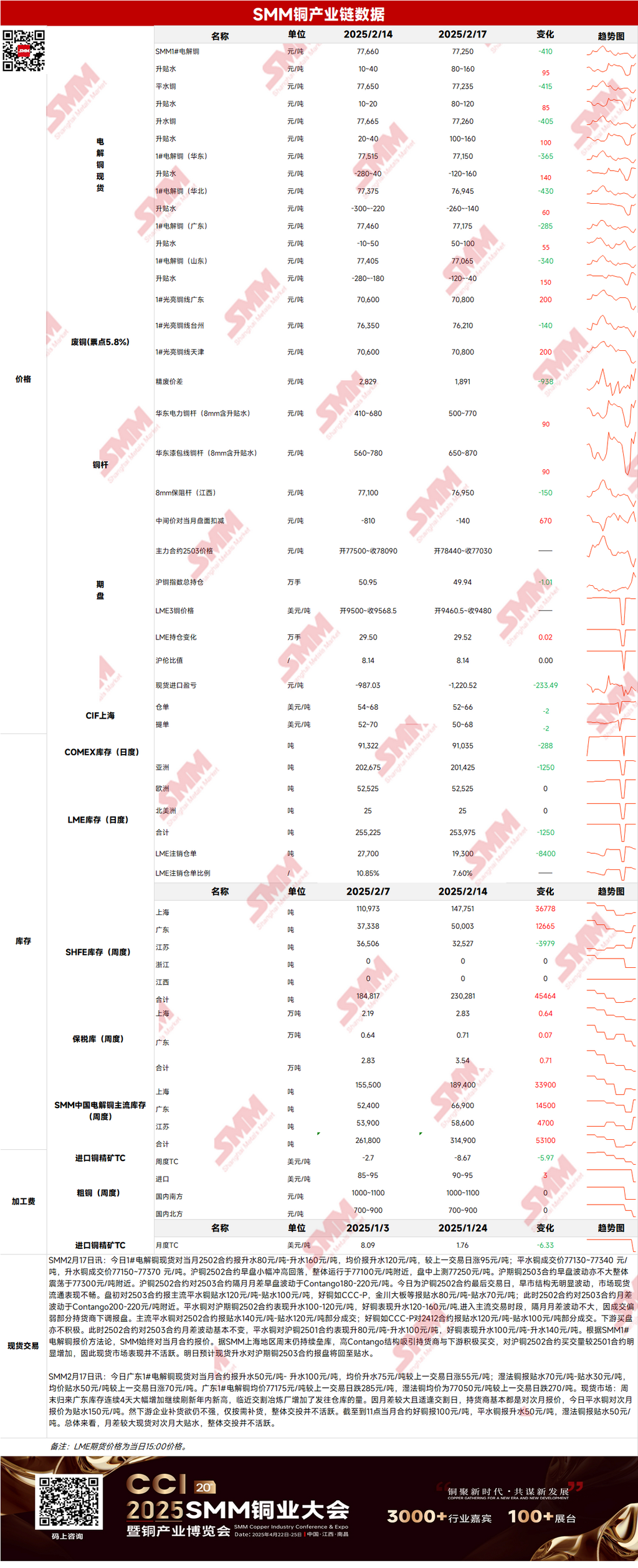

(2) As of Monday, February 17, SMM national mainstream regional inventories increased by 24,100 mt WoW to 350,300 mt, with total inventories up by 184,500 mt compared to the pre-holiday level of 165,800 mt.

Spot Market: (1) Shanghai: On February 17, #1 copper cathode spot premiums against the front-month 2502 contract were quoted at 80-160 yuan/mt, with an average premium of 120 yuan/mt, up 95 yuan/mt from the previous trading day. According to SMM, inventory buildup continued over the weekend in the Shanghai region. The high contango structure attracted active buying from suppliers and downstream, with trading volumes against the SHFE copper 2502 contract significantly higher than the 2501 contract. However, the spot market remained inactive. Spot premiums against the SHFE copper 2503 contract are expected to return to discounts today.

(2) Guangdong: On February 17, Guangdong #1 copper cathode spot premiums against the front-month contract were quoted at 50-100 yuan/mt, with an average premium of 75 yuan/mt, up 55 yuan/mt from the previous trading day. Overall, the large price spread between futures contracts led to significant discounts for spot prices against the next-month contract, resulting in subdued trading activity.

(3) Imported Copper: On February 17, warehouse warrant prices ranged from $52 to $66/mt, QP March, with an average price down $2/mt from the previous trading day. B/L prices ranged from $50 to $68/mt, QP March, with an average price down $2/mt. EQ copper (CIF B/L) was quoted at $1-15/mt, QP March, with an average price down $1/mt. Quotes referenced late February to early March arrivals. Yesterday, the SHFE/LME price ratio for the SHFE copper 2503 contract was around -700 yuan/mt. LME copper 3M-Mar contango was at C$38.91/mt, while the 2502-month date to 2503-month date backwardation was around $51/mt. After a brief shock last Friday evening, the near-month structure of LME copper turned to backwardation. Buyers and sellers were cautious yesterday, with limited market inquiries and offers.

(4) Secondary Copper: On February 17, secondary copper raw material prices rose by 200 yuan/mt MoM. Guangdong bare bright copper prices ranged from 70,700 to 70,900 yuan/mt, up 200 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 1,891 yuan/mt, down 938 yuan/mt MoM. The price difference for secondary copper rods was 775 yuan/mt. According to the SMM survey, the discount of secondary copper rod against copper futures narrowed significantly compared to last Friday. Communication with secondary copper rod enterprises revealed that most supplies are controlled by traders. Due to end-users' pessimistic consumption outlook, pre-holiday stockpiling was low, and high post-holiday copper prices suppressed restocking sentiment. Currently, end-users have resumed normal production and must procure raw materials. With limited market supply, secondary copper rod plants opted to stand firm on quotes.

(5) Inventory: On February 17, LME copper cathode inventories decreased by 1,250 mt to 253,975 mt. SHFE warrant inventories increased by 42,870 mt to 154,491 mt.

Prices: Macro side, US Fed - Harker stated that current economic conditions support maintaining a stable interest rate policy for now, while Bowman emphasized the need for stronger confidence in inflation decline before further rate cuts. Inflation is expected to decline, but upside risks remain. The US dollar index remained stable. After contract rollover, short covering subsided, and copper prices shifted lower. Fundamentals side, under the high contango structure, suppliers actively bought, but the spot market remained inactive. Downstream processing enterprises still expect copper prices to decline further. Overall, with the US dollar index fluctuating at low levels and major domestic meetings gradually unfolding, copper prices are expected to find support at the bottom today.

》Click to View the SMM Metal Database

【The above information is based on market data collected and comprehensive evaluations by the SMM research team. The information provided herein is for reference only and does not constitute direct investment advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】